Why we don't see Fed rate hikes anytime soon

Este artículo está disponible sólo en inglés.

The U.S. Federal Open Market Committee, the Federal Reserve's policy-setting panel, gets its broad marching orders from Congress. Its dual mandate is to steer the U.S. economy to both price stability and maximum sustainable employment. How the Fed uses its discretion in achieving these goals, as well as in defining them, is at the heart of its policy decisions—and it's why Vanguard believes the Fed is unlikely to raise rates in the near term.

The Fed has outlined changes to its monetary policy framework that give us confidence that it won't raise its benchmark federal funds rate target until at least 2023, even as stimulus payments flow through the economy and stock markets remain near record highs. On Wednesday, March 17, the Fed reaffirmed that it would keep monetary policy accommodative for the foreseeable future to support economic recovery from the COVID-19 pandemic. It said it would keep its rate target near zero and continue to increase its holdings of Treasury securities and agency mortgage-backed securities by a total of at least $120 billion per month for now.

In this Q&A, Vanguard economists Andrew Patterson and Adam Schickling discuss the conditions driving the Fed's decision-making, including its 2020 move to an average inflation target and Chairman Jerome Powell's view that maximum sustainable employment means people in historically hard-to-reach pockets of the labor market getting back to work.

First and foremost, what is Vanguard's view on recovery from the COVID-19 pandemic?

Mr. Patterson: We believe that health outcomes matter most to the pace of recovery. We've said this since it became clear just how hard the pandemic would hit the global economy, and we emphasized it in our Vanguard Economic and Market Outlook for 2021. The world is, thankfully, making progress against COVID-19, and optimism is building, but we haven't defeated it yet. Virus variants that may spread more easily have emerged in some places, and vaccine distribution in some parts of the world has been halting. But in the United States, more than two million vaccine doses per day are being administered—a pace that, as we wrote in January, would allow the U.S. to achieve COVID-19 herd immunity at some point this summer.1

As progress continues, economic activity could increase literally before our eyes. Restaurants and bars will fill up again as restrictions are relaxed and people become more comfortable engaging face to face. The just-enacted American Rescue Plan will put $1,400 in most Americans' pockets. And we expect economic outcomes to start changing, too, with inflation pressures rising and unemployment falling.

How is the Fed likely to respond to rising inflation pressures and falling unemployment?

Mr. Patterson: With patience! The Fed's definitions of stable prices and maximum sustainable employment—or full employment, as it's commonly called—allows for patience. The headline inflation and employment numbers will no doubt attract attention in the financial markets and the media. But as the Fed has explained, there's reason to look well beyond these headline numbers.2

What's the Fed's rationale for patience regarding the labor market?

Mr. Schickling: Broadly, the labor market has a long way to go before we can say it has recovered from the pandemic, and perhaps longer before we can say we've achieved full employment. The unemployment rate has come down significantly—to 6.2% in February 2021, from 14.8% in April 2020 upon the full onset of the pandemic. But the rate was 3.5% just before the pandemic, and we don't see it approaching that level before the end of 2022.3

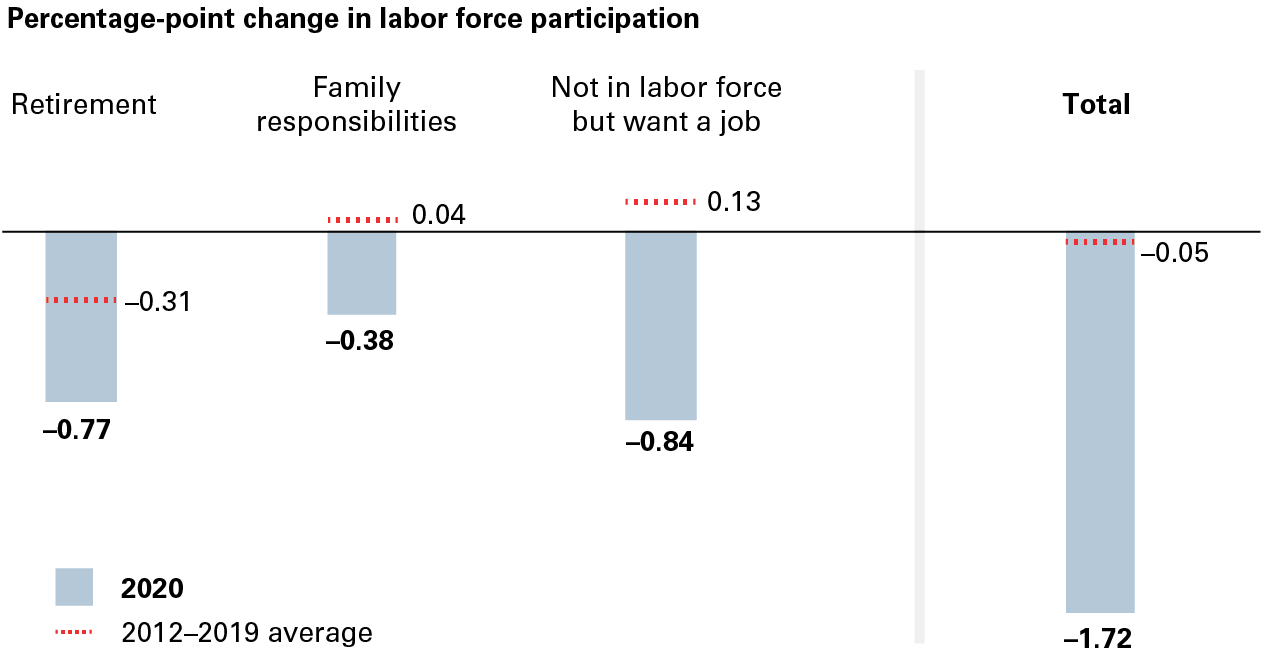

At this stage of the recovery, the headline unemployment rate provides little insight. Far more meaningful are factors such as the labor force participation rate, and that's down significantly, from 63.3% before the pandemic to 61.4% in February 2021. The difference in these numbers contains the stories of people knocked out of the workforce—parents caring for children whose classroom is now the kitchen table or people who lost a job and have given up hope of finding another one. We can attribute nearly a million early retirements to the pandemic that wouldn't otherwise have occurred. In the context of setting interest-rate targets, the Fed will consider not only broad employment numbers such as the unemployment rate, but also who's out of work and why.

How the pandemic has pushed people out of the labor force

Notes: The illustration reflects percentage-point changes in the U.S. labor force participation rate attributable to selected reasons for leaving or joining the workforce. Decreases reflect conditions that have kept people out of the labor market. Increases reflect an alleviation of these conditions.

Sources: Vanguard calculations, based on the U.S. Bureau of Labor Statistics' Current Population Surveys.

How does the Fed define full employment?

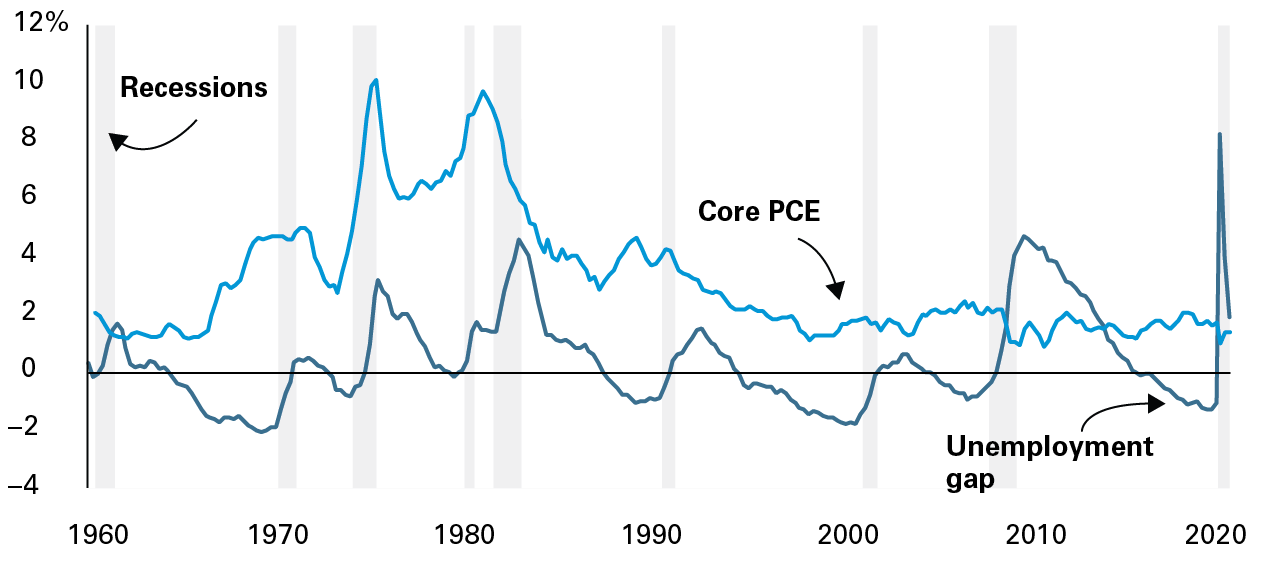

Mr. Schickling: The Fed's full-employment definition has evolved over the last decade or so, and that's instructive in considering when the Fed may feel a need to raise interest rates. Economists once considered estimates of NAIRU—a measure of the lowest the unemployment rate could go without triggering inflation—to generally be around 5%, and the Fed put significant emphasis on that number.4 Over the last 25 years, however, unemployment has periodically fallen below NAIRU without triggering worrisome inflation, meaning the relationship between unemployment and inflation has likely changed.

When now-U.S. Treasury Secretary Janet Yellen chaired the Fed from 2014 to 2018, she maintained a dashboard that considered, among other measures, job openings, layoffs, underemployment, and long-term joblessness to help determine how much slack remained in the labor market. Current Fed Chair Jerome Powell has made clear he is also seeking improvement in areas that are typically late to recover after a recession, such as labor force participation among workers without college degrees, wage growth for the lowest-paid workers, and Black unemployment. Mr. Powell's Fed wants full employment to reflect the full labor market, and rate hikes may not come until it clearly does, or will, reflect that.5

Tight labor markets haven't recently triggered worrisome inflation

Notes: The unemployment gap is the headline unemployment rate minus the non-accelerating inflation rate of unemployment (NAIRU). An unemployment gap below zero generally indicates a tight labor market. Core PCE is the U.S. Bureau of Economic Analysis's Personal Consumption Expenditures Price Index excluding volatile food and energy prices—the Federal Reserve's preferred measure of inflation. Recessions are as designated by the National Bureau of Economic Research, the de facto arbiter of U.S. economic recessions. Data through December 31, 2020.

Sources: Vanguard calculations, based on data from the U.S. Bureau of Labor Statistics, the U.S. Bureau of Economic Analysis, the U.S. Congressional Budget Office, and the National Bureau of Economic Research.

What about the Fed's rationale for patience in relation to inflation?

Mr. Patterson: The Fed made an important change to its approach last year to help anchor inflation expectations. It changed its inflation target from specifically 2% to an average of 2% over time. Such a change had been anticipated, as core inflation had been below 2% for so long.

The new approach seems tailor-made for a situation that we expect lies just ahead, in the second quarter of 2021 and beyond. When the pandemic slammed the broad economy a year ago, activity largely came to a standstill, bringing prices down, too. These base effects—comparisons to the low year-earlier prices—will magnify rises in core inflation in the months ahead, just as people begin to re-engage in face-to-face activities with stimulus cash in their pockets.

The new average inflation target gives the Fed a buffer to hold rates steady until it's confident that inflation will remain persistently around 2%. We expect an overshoot of 2% core inflation to be short-lived. And we expect the long-term structural trends that have kept inflation low for more than a decade—most notably technology and globalization—to continue to limit price rises, though we'll keep a close eye on the role inflation expectations may play.

What do the Fed's most recent economic projections show?

Mr. Patterson: The Fed updates its economic and policy-setting projections every other meeting. Its updates for the March 17 meeting were its first since December 2020. Although the new projections reflect more optimism about the pace of economic recovery, Federal Reserve Board members and Fed bank presidents collectively don't foresee both annualized core inflation surpassing 2% and the unemployment rate reaching pre-pandemic levels until 2023. And it's only beyond that when the majority of Federal Open Market Committee meeting participants foresee that they'd be likely to support raising the Fed's rate target.

How does Vanguard see the $1.9 trillion in new stimulus affecting U.S. growth and inflation?

Mr. Patterson: With the enactment of the stimulus bill, we project that the U.S. economy will register full-year growth in a range of around 7% to 7.5%. That's an eye-popping number for a country whose potential growth is estimated at around 2%, and it's an increase of 2 to 2.5 percentage points compared with our projection without the new stimulus. But for perspective, it's on the heels of a 3.5% decline in U.S. output in 2020, because of the pandemic.6

We believe that the stimulus legislation's direct effect on inflation is likely to be modest, around 7 to 10 basis points for all of 2021.7 As I alluded to earlier, inflation expectations present a risk to our view because heightened expectations can materially affect actual inflation. This is where the Fed will need to be visible, acknowledging expectations and managing them through careful guidance on its views. For the foreseeable future, we expect its guidance to be that the labor market has a long road to recovery, that inflation expectations remain anchored, and that rate hikes remain relatively distant.

1 According to the Bloomberg COVID-19 Vaccine Tracker, an average of 2.47 million vaccine doses per day were administered in the United States in the week ended March 17.

2 Good examples of the Fed's public communications on this point are a January 13, 2021, speech on full employment by Fed Governor Lael Brainard, available at federalreserve.gov/newsevents/speech/brainard20210113a.htm, and a January 13, 2021, speech by Fed Vice Chair Richard Clarida on price stability, available at federalreserve.gov/newsevents/speech/clarida20210113a.htm.

3 Unemployment and labor force participation data are from the U.S. Bureau of Labor Statistics.

4 NAIRU stands for non-accelerating inflation rate of unemployment.

5 For example, see Fed Chair Jerome Powell's February 10, 2021, speech on the labor market, available at federalreserve.gov/newsevents/speech/powell20210210a.htm.

6 This figure measuring the 2020 U.S. change in real GDP is from the U.S. Bureau of Economic Analysis, second estimate, February 25, 2021.

7 A basis point is one-hundredth of a percentage point.

Notes:

- All investing is subject to risk, including the possible loss of the money you invest.

- For institutional and sophisticated investors only. Not for public distribution.

Important information

VIGM, S.A. de C.V. Asesor en Inversiones Independiente (“Vanguard Mexico”) registration number: 30119-001-(14831)-19/09/2018. The registration of Vanguard Mexico before the Comisión Nacional Bancaria y de Valores (“CNBV”) as an Asesor en Inversiones Independiente is not a certification of Vanguard Mexico's compliance with regulation applicable to Advisory Investment Services (Servicios de Inversión Asesorados) nor a certification on the accuracy of the information provided herein. The supervision scope of the CNBV is limited to Advisory Investment Services only and not all services provided by Vanguard Mexico.

This material is solely for informational purposes and does not constitute an offer or solicitation to sell or a solicitation of an offer to buy any security, nor shall any such securities be offered or sold to any person, in any jurisdiction in which an offer, solicitation, purchase or sale would be unlawful under the securities law of that jurisdiction. Reliance upon information in this material is at the sole discretion of the reader.

Securities information provided in this document must be reviewed together with the offering information of each of the securities which may be found on Vanguard's website: https://www.vanguardmexico.com or www.vanguard.com

Vanguard Mexico may recommend products of The Vanguard Group Inc. and its affiliates and such affiliates and their clients may maintain positions in the securities recommended by Vanguard Mexico.

ETF Shares can be bought and sold only through a broker and cannot be redeemed with the issuing fund other than in very large aggregations. Investing in ETFs entails stockbroker commission and a bid-offer spread which should be considered fully before investing. The market price of ETF Shares may be more or less than net asset value.

All investments are subject to risk, including the possible loss of the money you invest. Investments in bond funds are subject to interest rate, credit, and inflation risk. Governmental backing of securities apply only to the underlying securities and does not prevent share-price fluctuations. High-yield bonds generally have medium- and lower-range credit quality ratings and are therefore subject to a higher level of credit risk than bonds with higher credit quality ratings.

There is no guarantee that any forecasts made will come to pass. Past performance is no guarantee of future results.

Prices of mid- and small-cap stocks often fluctuate more than those of large-company stocks. Funds that concentrate on a relatively narrow market sector face the risk of higher share-price volatility. Stocks of companies are subject to national and regional political and economic risks and to the risk of currency fluctuations, these risks are especially high in emerging markets. Changes in exchange rates may have an adverse effect on the value, price or income of a fund.

The information contained in this material derived from third-party sources is deemed reliable, however Vanguard Mexico and The Vanguard Group Inc. are not responsible and do not guarantee the completeness or accuracy of such information.

This document should not be considered as an investment recommendation, a recommendation can only be provided by Vanguard Mexico upon completion of the relevant profiling and legal processes.

This document is for educational purposes only and does not take into consideration your background and specific circumstances nor any other investment profiling circumstances that could be material for taking an investment decision. We recommend to obtain professional advice based on your individual circumstances before taking an investment decision.